Over the last 18-20 months, The COVID-19 pandemic has disrupted virtually every market in this country. From the investment space, healthcare industry, and real estate market, once predictable industries have become an incredibly volatile, wild domain. Living spaces turned into our workplace, online communication channels and teleconferencing software such as Zoom and Microsoft Teams have been used to conduct business and family reunions alike, and slow-moving shifts in our pre-pandemic economy have been greatly accelerated.

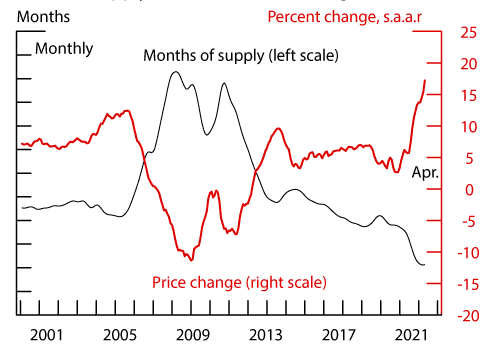

According to the Federal Reserve, the COVID-19 pandemic has caused the housing market to tighten considerably. The figure below shows that the months’ supply of homes for sale has fallen to historically low levels. Related to this tightness, the figure also shows that house price growth has increased substantially during the pandemic. The tighter housing market could reflect increased demand (higher inflow of buyers to the market), reduced supply (lower inflow of sellers to the market), or some combination of the two.

On our blog this year, we have discussed the difference between home-buying vs. renting, the significance of a credit score for renters, and why it is important to hire a real estate professional as a new homeowner. Wherever you are in the process of home-buying, it is crucial to understand the current trends in the housing market to be better prepared for your next move.

One short year and a half ago, millions of busy Americans abruptly halted their morning routine and were involuntarily remanded to their homes to continue working, socializing, and conducting normal activities, although remotely. This shift in norms catalyzed the desire for families to purchase larger homes. According to Forbes, the housing supply was already low before COVID-19, but it was further hampered as lockdowns took place and people began looking for new homes, driven by a host of reasons—from the desire to leave populated cities to better home offices. The Federal Reserve took steps to keep the financial markets liquid and to ensure mortgage rates stayed low. However, these low mortgage rates pale in comparison to soaring housing prices in the past year. Home prices nationwide, including distressed sales, grew by 17.2% in June 2021 compared with June 2020—a record high, according to the latest CoreLogic report.

Low mortgage rates (a 30-year fixed-rate mortgage was 3.02% in June, dropping even lower to 2.78% in July), along with an increase in work-from-home opportunities have fueled a surge in housing demand, particularly in lower-density suburbs. Millennials in this country flocked out of the inner city and into the suburbs, causing home prices to skyrocket. The high demand caused inventory to plummet, which has caused a shortage.

Although there is still a very high demand for homebuyers, the shortage of inventory and home supplies is keeping many buyers at bay until these prices decrease. Because of the increase in millennial homeownership, growing construction costs, and real-estate investors scooping up starter houses, the housing supply is presently at its lowest level since the 1970s. To keep on top of these trends, check out the National Association of Realtors housing shortage tracker here.